The growth momentum in China has shown signs of weakness as seen by recent economic data. For example, the September NBS manufacturing PMI declined to 50.8 from 51.3 in August, with major sub-indexes edging down1.

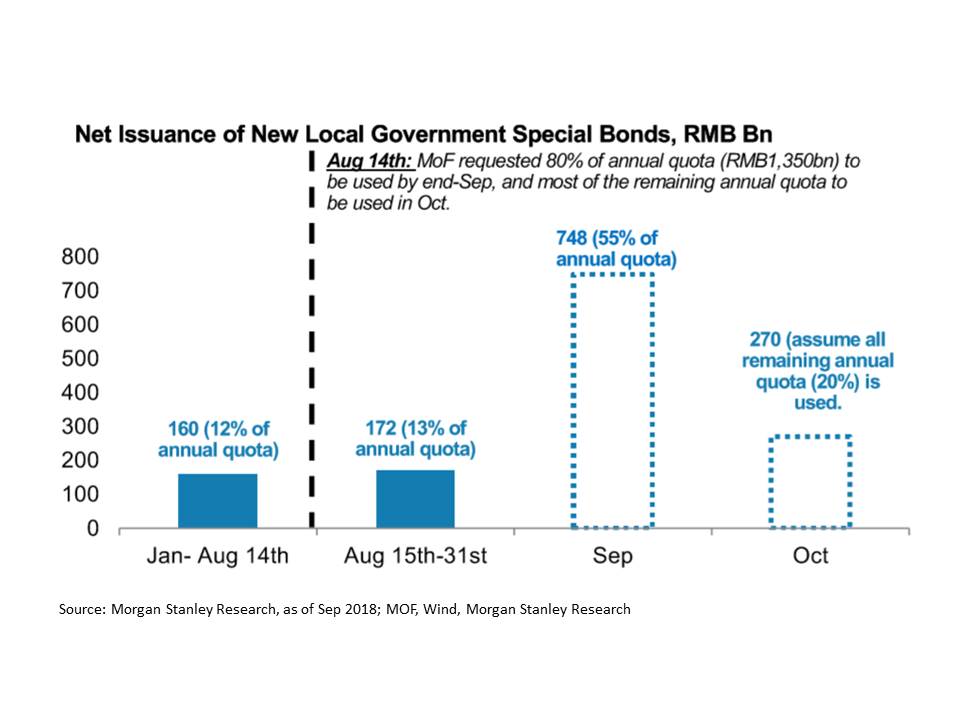

On Oct. 7, the PBoC announced the fourth reserve requirement ratio (RRR) cut this year, cutting by 100bps which reduces the RRR for large banks to 14.5%2. The amount of liquidity released from this cut will likely amount to Rmb 1.2trn2. Rmb 450bn will be used to replace the Medium-term Lending Facility that is maturing in October, while the rest will be used to support liquidity, and we believe this will alleviate funding pressure from tax submission in October2. We think the effect of RRR cut is limited, as evident by the slumping SHIBOR rates, indicating the unwillingness of banks to make new loans to the real economy despite sufficient liquidity. Nonetheless, the RRR cut may help local governments sell more bonds to banks. Bond issuances are expected to peak between 3Q and 4Q which may boost total social financing and infrastructure investment in 4Q18 and next year. In addition, we believe more fiscal and monetary policies will be released in the coming months as the Minister of Finance announced that he is studying tax cuts possibilities. Finally, while the RRR cut will add to RMB depreciation pressure, we believe the central government has placed higher priority on tackling internal challenges over external uncertainties at this juncture, and therefore should be determined to avoid high fluctuation of RMB exchange via stringent capital control for the rest of 2018.

Although we’ve shifted to a more conservative strategy in volatile markets, we stay very alert to the possibility that the tide could turn when the government initiates more aggressive measures to support the economy. The Fourth Party Plenum of the 19th Party Congress is scheduled to take place around the latter half of November. We expect the government to form internal consensus on how strong the stimulus measures should be implemented. For instance, VAT rate cut could be an effective tool to boost consumption and GDP. We estimate that for every 1% cut in VAT, there would be RMB520bn (0.6% GDP boost) worth of tax savings to the general public3. Additionally, for every 1% rate cut of social security contribution by corporates and/or individuals would reduce their burdens by Rmb250-300bn3. We consider various tax reductions to be much more direct and powerful tools to support the real economy than RRR cuts, and we believe that the government will implement those measures when necessary.

[1] Source: National Bureau of Statistics, as of September 2018

[2]Source: BNP Paribas, as of October 2018

[3]Source: Zeal Asset Management Limited, as of October 2018

This document is based on management forecasts and reflects prevailing conditions and our views as of this date, all of which are accordingly subject to change. In preparing this document, we have relied upon and assumed without independent verification, the accuracy and completeness of all information available from public sources. All opinions or estimates contained in this document are entirely Zeal Asset Management Limited’s judgment as of the date of this document and are subject to change without notice.

Investments involve risks. You may lose part or all of your investment. You should not make an investment decision solely based on this information. If you have any queries, please contact your financial advisor and seek professional advice. This document is issued by Zeal Asset Management Limited and has not been reviewed by the Securities and Futures Commission in Hong Kong.